President Donald Trump’s tariffs on Canada and Mexico are an “attempt to stop the bleeding” in the American economy, United Auto Workers President Shawn Fain said on “This Week” on Sunday, defending the controversial measures.

“We’re in a crisis mode in this country,” Fain stated, arguing that America’s trade system is “broken” and in need of significant reform. “We’re in a triage situation,” he added.

Tariffs “aren’t the end solution,” Fain explained, “but they are a huge factor in fixing this problem.”

“Tariffs are an attempt to stop the bleeding from the hemorrhaging of jobs in America for the last 33 years,” Fain said, asserting that the U.S. had lost “millions of jobs” since the North American Free Trade Agreement (NAFTA) took effect in 1994. “NAFTA sucks,” Fain declared.

“The United States is the market everyone wants to sell in, and we should have reciprocal trade laws where people have the same standard of living,” he continued.

“Our neighbors to the south—Mexican workers—aren’t the enemy. They’re being exploited, and it’s because of corporate greed, and that’s what’s got to stop,” he said.

The Trump administration announced last week that it would implement 25% tariffs on auto-related goods from Mexico and Canada.

However, after discussions between Trump and executives from Ford, General Motors, and Stellantis, the administration decided to delay the measures by one month. The tariffs are now set to take effect in April.

White House press secretary Karoline Leavitt stated that the president instructed the companies to “start investing, start moving, shift production here.”

The UAW—which represents around 1 million members—has long advocated for bringing jobs and manufacturing back to the U.S. The organization has expressed support for Trump’s decision to impose tariffs.

“Tariffs are a powerful tool in the toolbox for undoing the injustice of anti-worker trade deals,” the union said in a statement posted to its website on Tuesday. “We are glad to see an American president take aggressive action on ending the free trade disaster that has dropped like a bomb on the working class.”

The UAW has argued that any resulting price increases for consumers would be the fault of corporations rather than the president.

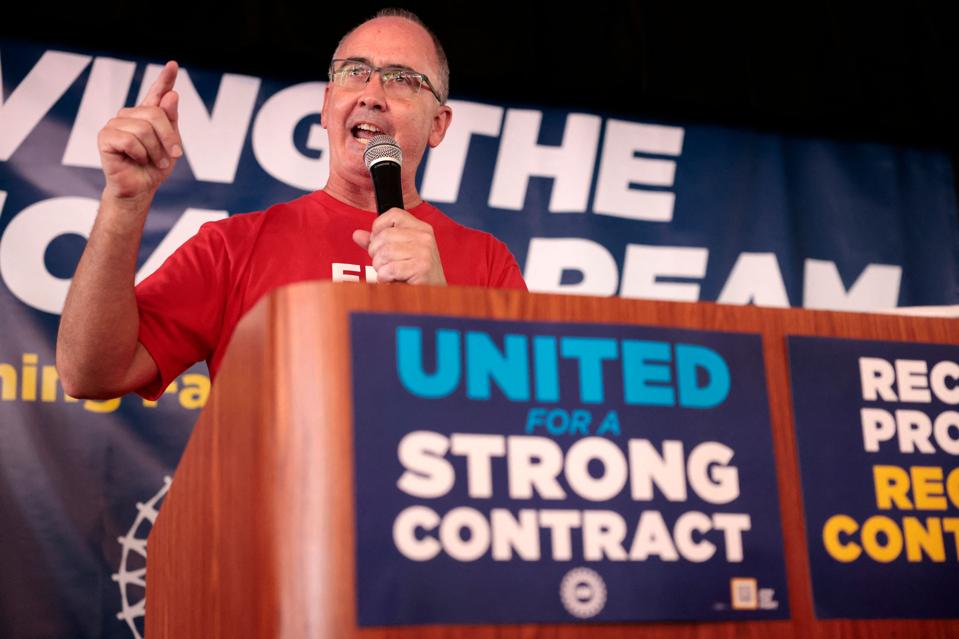

UAW President Shawn Fain

UAW President Shawn Fain“There’s been a lot of talk of these tariffs ‘disrupting’ the economy,” the UAW said in its statement last week.

“But if corporate America chooses to price-gouge the American consumer or attack the American worker because they don’t want to pay their fair share, corporate America bears the blame for that decision.”

The UAW endorsed Democratic candidate Kamala Harris in the 2024 election. Fain had previously called Trump a “scab.”

Since Trump’s reelection, however, the union’s stance has shifted. Last week, the UAW stated that it was in “active negotiations with the Trump administration about their plans to end the free trade disaster.”

“We look forward to working with the White House to shape the auto tariffs in April to benefit the working class,” the union added.

Fain has been outspoken in his criticism of various aspects of the Trump administration, particularly regarding the influence of billionaire Elon Musk.

Speaking at a “fighting oligarchy” event in Warren, Michigan, last week, Fain denounced Musk’s attacks on Social Security.

“It’s not our grandparents, and it’s not a public school teacher,” Fain said. “It’s Elon Musk and the billionaire class. And you want to talk about a Ponzi scheme? I’ll tell you about a Ponzi scheme.

The only Ponzi scheme we’ve seen in the last 40 years is the rich getting richer while the working class and everyone else gets left behind.”

On “This Week,” Fain emphasized the importance of moving forward despite past disagreements. “The election is over.

Donald Trump is the president, and we want to get to work to fix the problems that are wrong with this country, with our economy. And the American people expect that. They expect leaders to stand up and lead. They don’t expect us to sit back.”